An equity portfolio "with no room for passengers"

A number of firms with hedge fund backgrounds have found success in expanding into long-only strategies in SA. I chatted to Steyn Capital's Andre Steyn about how they have got this right.

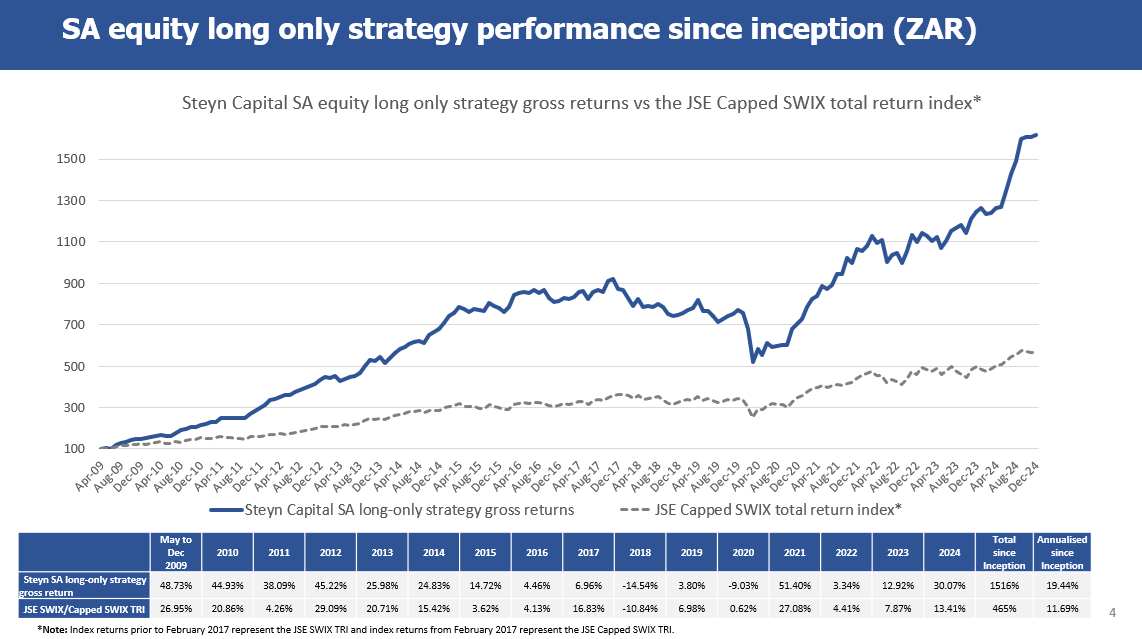

Since its inception in 2009, Steyn Capital’s long-only SA equity strategy has returned an impressive 19.44% per annum. The strategy, which is also available in CIS form through the Steyn Capital Equity Prescient Fund, enjoyed some early outsized returns, but has also been a standout performer more recently.

In 2021, the strategy was up 51.4%, against the 27.1% gain in its Capped Swix benchmark. And in 2024 it returned 30.1% when the Capped Swix was up 13.4%.

Source: Steyn Capital

Portfolio manager Andre Steyn explains that the strategy leverages off the firm’s hedge fund expertise. He says that it is almost a replica of the long book of the firm’s highly successful hedge fund, with certain risk adjustments.

“We are able to do that because we build the longs and shorts in our hedge fund very differently,” Steyn says. “On the long side, what is important is quality and valuation. On the short side, valuation is unimportant. Catalysts are important. So, we build them on a standalone fashion.

“That translates into the long-only unit trust being built in a benchmark agnostic fashion as a portfolio of our best ideas.”

“The active share is typically 65% to 70%.”

He adds that there is “no room for passengers” in the portfolio. He only wants to include stocks where they feel they have an investment edge.

“The active share is typically 65% to 70%,” Steyn says. “That makes it a good portfolio for people who want to blend it with a passive exposure.”

He says that the minor differences between the long-only portfolio and the long book of the hedge fund are due to excluding “risk items that we don’t necessarily want to take on”.

“For example, in 2021 we had Thungela as a big long position in the hedge fund, but we held a smaller position in the long-only portfolio only because we were short Exarro in the hedge fund. That wasn’t constructed as a pair trade, but we were hedging some coal price risk by doing it, and for that reason we were able to carry a much bigger position in the hedge fund.”

While Steyn (pictured above) emphasises that the portfolio is constructed bottom-up without reference to the benchmark, the weight that a stock holds in the index may influence position sizing.

“Our position sizing has always worked with reference to a stock’s upside price potential, its downside price risk, the conviction level we give it ranging between one and 10, and stock-level liquidity,” Steyn says. “But since 2019 or so, we also look at the size of the stock in the benchmark.

“It’s something we’ve learned to consider when we’re positive on a stock because in 2017 we were positive Naspers, but only had a 3% position. That might have been meaningful in the portfolio, but it turned out to be massively underweight. The stock was up two-thirds that year, but it was our biggest relative detractor.

“Now when we like something, we don’t want to be massively underweight.”

Mid and small cap exposure

The portfolio typically holds between 35 and 40 stocks, and it looks across the market cap spectrum.

“Of the R15.5 billion we manage, R11.5 billion is in SA, and I feel we are most definitely a boutique,” Steyn says. “We are big enough to afford the resources to do very high-quality work, but small enough to have real positions in the top 140 to 150 stocks.

“That is definitely one of our advantages. Being able to have meaningful 3%-type positions down to mid-caps and small-caps has been a benefit to us over time.”

“It’s almost like we have two stock markets in South Africa.”

Illustrating this is that the fund’s largest holding currently is Southern Sun.

“It’s almost like we have two stock markets in South Africa,” Steyn says. “There is a large cap market where valuations are higher and liquidity is plentiful. And then you have the rest.

“We hold a combination between of large cap liquid stocks like FirstRand, Shoprite and Glencore, and SA Inc. exposure like Southern Sun, Sun International and Premier Foods.”

“Dispassionate approach”

He adds that in both cases, the firm’s focus is the same.

“Our bread and butter is owning high-quality businesses that are undervalued.”

This is achieved first of all through an idea generation engine developed off the back of Steyn’s own experience in running hedge funds internationally.

“We have analysts going over financial statements by hand.”

“I saw various ways of generating ideas, and what resonated with me is having a dispassionate approach,” he says. “Utilise academic research to lead you to what should outperform, and marry that with cleaned up data.

“We have analysts going over financial statements by hand, looking for high quality earnings, hidden assets, hidden liabilities and extraneous items.”

The firm builds valuation models for different types of businesses using different metrics. For operating businesses, for example, it looks at enterprise value over earnings before interest and tax (EV/EBIT). It then equally weights a quality proxy, which is usually return on invested capital (ROIC).

“To get that ROIC, we look at only assets a company is using to generate a return,” Steyn says. “When we invested in Grindrod, for example, they had a variety of non-core assets they were looking to dispose of that yielded no return. One of those was a large tract of land in KwaZulu-Natal they sold for half a billion rand.

“You need to remove that from earning assets to get a true picture.”