Getting risk management right in a global quality growth portfolio

The Guinness Global Innovator's Fund has a track record of capturing growth upside with less downside risk. Co-portfolio manager Ian Mortimer explains how they get that right.

Investors with a growth bias have had a tough start to the year. The MSCI World Growth Index was down 7.5% in March alone, far outpacing the 4.4% decline in the MSCI World Index that month.

Much of this weakness was concentrated in the US. The MSCI USA Growth Index was off 9.1% in March.

“Part of that US underperformance was clearly due to the stock-specific risk that we’ve seen build up in the US index with some of those large US tech companies just becoming bigger and bigger parts of that market,” says Ian Mortimer, co-portfolio manager of the Guinness Global Innovators Fund.

This was seen more broadly in the relative performance of US and European markets as a whole. While the MSCI Europe ex-UK Index gained over 11% in the first quarter, the MSCI USA Index was down over 4%.

Source: Guinness Global Investors & Bloomberg

“We saw a 15% delta between those two regions,” Mortimer says. “That was something we have not seen for a significant period of time.”

There were also stark differences in the performance of investment styles. The MSCI World Value Index was up around 5% for the quarter in US dollars, while the MSCI World Growth Index fell nearly 8%.

Source: Guinness Global Investors & Bloomberg

As a quality growth strategy, the Guinness Global Innovators Fund was understandably caught in the downdraught. The portfolio was down 3.7%, compared to the 1.8% decline in the MSCI World Index.

However, it meaningfully outperformed the MSCI World Growth Index.

Risk management

Mortimer explains that because the fund has a relatively high beta, seeing a drawdown when the market has fallen was “broadly what we might expect”. However, he adds that it is significant that the fund outperformed its benchmark growth index, which he put down to how they manage stock-specific risk.

“We run a 30-stock, equally-weighted portfolio,” he says. “That means that position sizes are typically around 3.3%.

“That means that we’ve been taking profits in many of the companies that were performing strongly. With Nvidia, for example, we rebalanced and took profits five times through 2024. Therefore, coming into this year, we were not overweight or even equal weight many of those big names that have been dominating the benchmark.”

“Managing that stock-specific risk is going to be critical.”

On a relative basis, that meant that as these large stocks sold off aggressively, the Guinness portfolio was not as heavily affected.

“I think that still remains quite important in today’s market environment,” Mortimer says. “Managing that stock-specific risk is going to be critical.”

This rebalancing doesn’t happen mechanically. The fund managers debate when to take the opportunity to sell down a holding that has run or to top up one that has underperformed. That means that they do allow weightings to drift.

At the end of March, for example, the fund held 4.1% of its portfolio in the London Stock Exchange and just over 2% in Novo Nordisk.

“But what you don’t see is companies at 8% or 9% of the portfolio,” Mortimer (pictured above) says. “Generally speaking, we keep holdings below the 5% level, even if they perform strongly.”

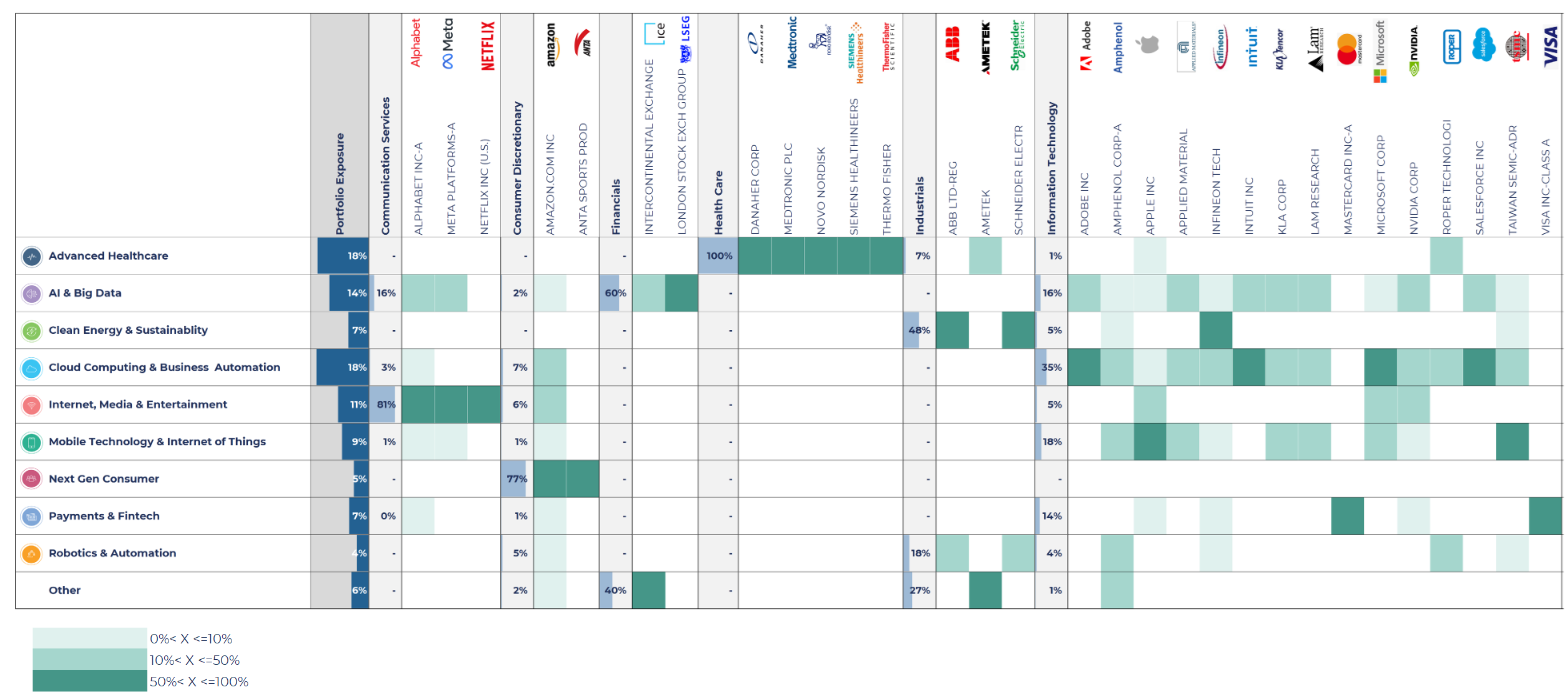

In a similar vein, the portfolio managers look to ensure diversification both within and across sectors.

“At the moment, we maintain a significant overweight to information technology, but we try to balance that across the three industries of semiconductors, software and hardware,” Mortimer says. “They are very different in terms of their business drivers and economic sensitivity.

Source: Guinness Global Investors

The fund also has over 10% exposure to financials, healthcare, communications services and industrials.

“We’re a little underweight consumer discretionary and hold no consumer staples,” Mortimer says. “We generally have a zero allocation to materials, utilities, real estate and energy, where we don’t find a lot of ideas.”

The portfolio managers also think about diversification in terms of different business drivers.

Source: Guinness Global Investors

“We’re trying to find companies that can grow their earnings faster than the market. We think that is the characteristic that drives outperformance,” Mortimer says.

“But that’s a pretty hard thing to predict. So, we start by looking for secular growth themes, and then for companies with exposure to those. Then we apply quality cutoffs so that we’re not just chasing interesting stories, but actually buying good businesses. Finally, we conduct a bottom-up valuation to make sure we’re not paying too much.

“We put that all together in our 30-stock portfolio, but we also look at that portfolio and ask what economic exposure do we have to different things? We don’t try to fill buckets to make sure we something in each theme, but we do want to see diversification.”