Outperforming in fixed income by removing “a big blindspot”

The PortfolioMetrix BCI Dynamic Income Fund stands out amongst income funds for often taking much longer duration. I chatted to portfolio manager Phil Bradford about how this approach came about.

The PortfolioMetrix BCI Dynamic Income Fund has consistently been one of the top-performing multi-asset income funds in South Africa. It has returned over 10% per annum and is the number one performing fund since its inception in December 2020.

Source: Morningstar, PortfolioMetrix as of 30/04/2025

The fund has a reputation for holding longer duration than many of its peers, but lead portfolio manager Philip Bradford says that the objective of the portfolio is not simply “to be a high-octane income fund all the time”.

“Our duration profile has frequently changed based on the opportunities and risks in the market,” he says. “Going into the end of 2020, for instance, we reduced bond exposure dramatically. Then again, before the Russian invasion of Ukraine in 2022 we had very little bonds, and a duration of only 0.8. We were getting better yields out of corporate bonds at the time. But when it made sense to do so, we increased duration significantly again, up to the current level of 3.7.”

Bradford adds that in the way the team runs the strategy, they see themselves as delivering asset allocation, rather than simply a “cash-plus” product.

“The opportunity we see is to span across everything.”

“There are only 20 bonds in the ALBI, all fixed-rate and almost entirely government issued. Then there are over 2,600 other bond instruments listed on the JSE, most of which don’t trade frequently, and this is where most income funds invest.

“But really the opportunity we see is to span across everything. We are doing asset allocation in the fixed income space. That is our focus, not because we wanted to be different but because we saw a blind spot.”

This “blind spot”, he believes, is a function of the history of the market.

Market evolution

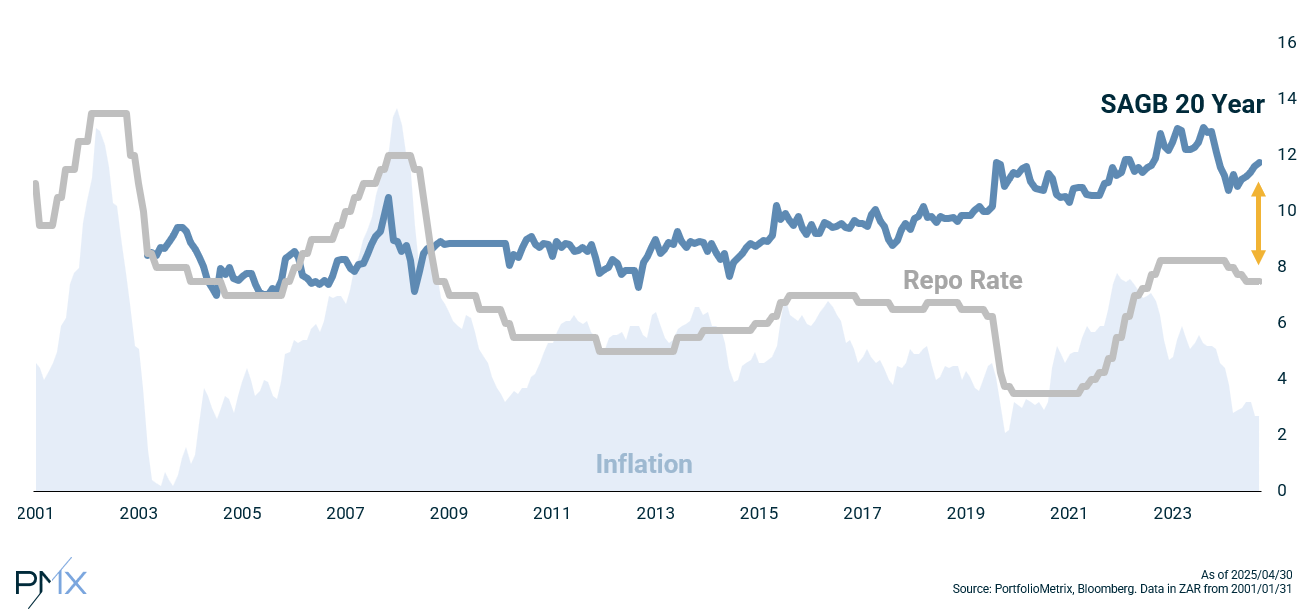

“Fifteen to 20 years ago, interest rates were very high, bond yields were very low, and you could get higher yields out of corporate credit,” Bradford says. “At the time, you were getting 12% from cash, while bond yields were 7% or 8%.

“You were getting 4% less than cash out of bonds for structural reasons: the government wasn’t borrowing and there was excess demand for its bonds. The yield curve was inverted because of this supply-demand imbalance.”

The upshot of this was that income fund managers – quite rationally in Bradford’s view – moved heavily into corporate credit, which is also predominantly floating-rate and therefore with very low duration.

“You could get 13% out of bank bonds that behaved like cash and only 8% from government bonds, so why would you buy government debt?” Bradford (pictured above) says. “Around R800 billion then moved into income funds, where everyone became specialised in credit. They got given mandates with a cash-plus return target, and low capital volatility constraint.”

However, the environment has since changed completely. Long-term bond yields have moved as high as 13% at times in recent years, while credit spreads have compressed and the repo rate has largely been around 7% for more than a decade.

“The opportunity set has subsequently shifted, but many managers find themselves boxed in by mandates that don’t allow capital volatility,” Bradford says. “But the least risky bonds from a credit perspective ironically happen to be the most volatile.

“This is an anomaly in the South African market right now. Part of it is driven by the wall of money still given to mandates that target a cash-plus type return. Over time, we have been able to outperform simply because we are prepared to accept this higher volatility.”

That’s not to say that the fund has no regard for how much duration it holds or standard deviation metrics. PortfolioMetrix uses a combination of instruments to build a portfolio that delivers a high yield at meaningfully lower volatility than the ALBI.

“If we wanted to buy more government bonds today, we could,” Bradford says. “But that would increase the volatility and not increase the yield much.”

Currently 45% of the portfolio is directly in fixed-rate government bonds.

Source: Morningstar, PortfolioMetrix as of 30/04/2025

“In bonds, credit risk is the most important thing,” Bradford says. “When you’re lending someone money, it’s not the volatility of the capital that matters most – it’s whether they can pay you back.

“The most creditworthy issuer in the country is still the government, and then the banks. The government also can’t let the major banks go bust. But with normal corporates, no one is bailing you out if something goes wrong.”

This informs how PortfolioMetrix approaches constructing the portfolio.

Identifying opportunity

“Credit risk is our first, most important decision. Then we look at what is the best yield we can get. If that happens to be out of the best credit quality assets, but we just need to lock it away a bit longer and take some volatility, we think that makes sense.

“It’s just a function of our market right now that that’s the opportunity,” Bradford says. “At some point in the future, I expect to reduce government fixed-rate exposure and move more into bank and government floating rate debt.”

“We are looking at what is going to be our best return out of thousands of combinations.”

He adds that if the yield curve inverted again like it did in 2008 and 2009, the portfolio would probably look completely different, with no fixed-rate government bond exposure.

“We are looking at what is going to be our best return out of thousands of combinations over the next two years, one year, six months,” Bradford says.

“We think that if you start at one or two year time horizon, our positioning should produce the best result. But if you start by saying you can’t tolerate any capital volatility over the next 3 months, you create a huge blind spot.”