The manager burning down the haystack to find the needle

The recently launched Bellamont BCI Global Equity Feeder Fund feeds into a novel global quality strategy run by Finnish firm Sifter. I thought it was worth finding out more.

South African investors haven’t had much exposure to Nordic fund managers. The Bellamont BCI Global Equity Feeder Fund that launched in May last year is therefore a refreshing standout.

The fund feeds into the Sifter Fund Global UCITS, run by the Helsinki-based asset management boutique Sifter.

“We look after private clients and believe quality as a style resonates with them because your drawdown capture is less and you have the ability to compound consistently,” explains Bellamont Group managing director Warren Quin.

“Not all the best managers can live in New York or London”

In Bellamont’s search to find a manager that could deliver persistent alpha through a quality approach, the firm made a conscious effort to broaden its search beyond just the UK and the US.

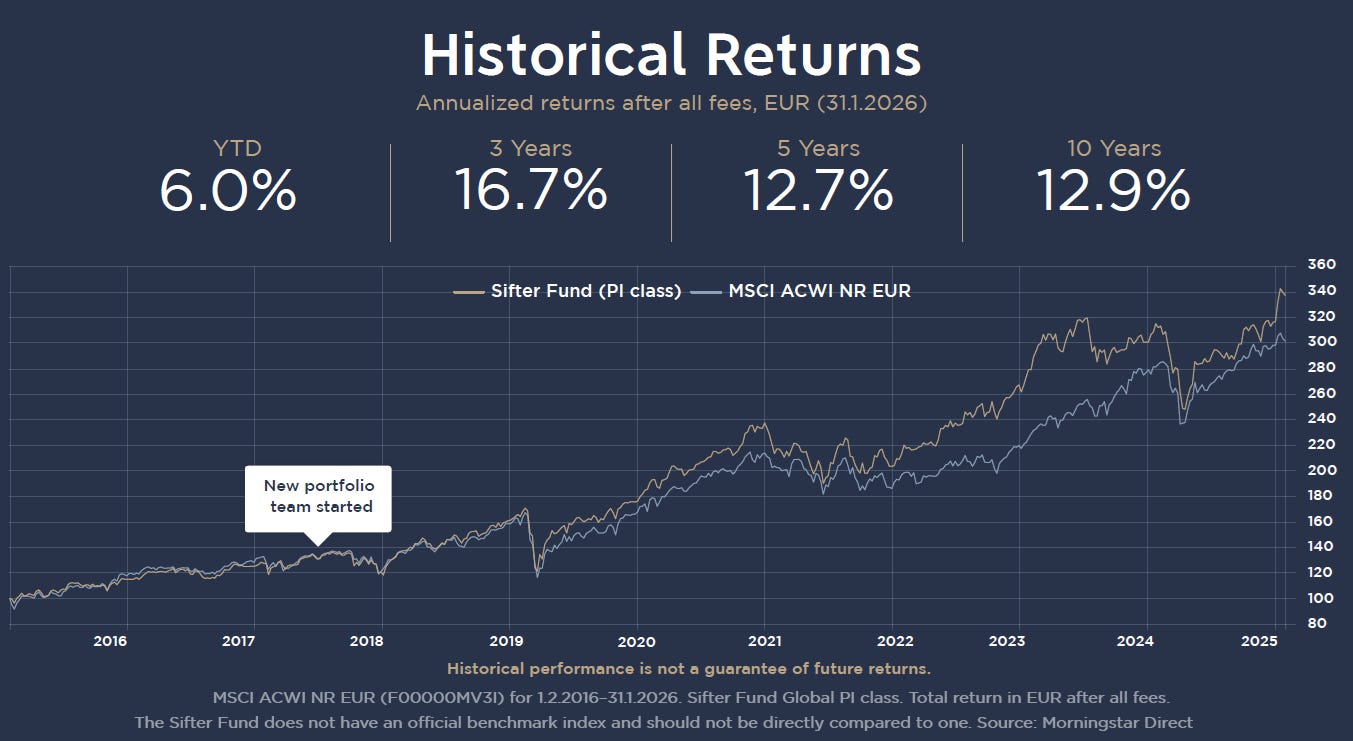

“Not all the best managers can live in New York or London,” Quin says. “We cast the net around the world, and that’s how we came across the Sifter fund which met all the criteria we were looking for. Most importantly, they are singly focused on this one strategy, and have a 20-year track record of delivering alpha to clients.”

Sifter CEO Santeri Korpinen says that the firm’s approach is defined by the fact that “instead of picking stocks, we eliminate them”.

“Our process is one of elimination, one of burning down the haystack to find the needle,” he says.

“Our investment universe consists of 65,000 companies worldwide. Through our proprietary screening system, we eliminate more than 99% of them to focus only on businesses with sustainable competitive advantages, strong balance sheets, and predictable earnings.”

This quant screen allows Sifter’s analysts to spend time only looking at genuine prospects.

“Eliminating stocks versus picking stocks may sound like a subtle nuance, but it contains a great deal of experience-based wisdom,” Korpinen (pictured below) adds. “Sifter’s founder, Dr. Hannes Kulvik, learned already in the 1990s during his time in Private Equity that investment opportunities often arrive sequentially not simultaneously.

“This challenge is known in economics as the ‘optimal stopping problem’, where an investor cannot compare opportunities side by side. Instead, decisions must be made one at a time.”

By eliminating the vast majority of the universe as quickly and objectively as possible, Sifter’s team is able to compare those that remain rigorously against each other.

“In this process, the stronger business model prevails and the weaker one is rejected,” Korpinen says. “A key advantage of this model is that it minimises the risks associated with trends, themes, market timing, and opportunistic decision-making.”

From the 500 companies that make it through Sifter’s screen, around 50 are analysed in depth every year. Only three to five of these will make it into the portfolio of between 25 and 30 counters.

“We don’t care about share price volatility, but the volatility of business returns.”

“We believe concentration reduces risks,” says portfolio manager Olli Pöyhönen. “We don’t care about share price volatility, but the volatility of business returns. And if we have 25 to 30 holdings, we can much more easily follow industry dynamics, monitor competitive advantages and check how companies are performing.”

Pöyhönen adds that Sifter’s stock selection focuses on four key pillars:

Growth that can be reinvested

At returns above the cost of capital

Protected by durable competitive advantages

At a reasonable valuation

“To get to a valuation we estimate a reasonable level of earnings the company can achieve five years from now and compare that to current capitalisation,” Pöyhönen (pictured below) says. “That allows us to see past market cycles that can be significant on an annual basis, but tend to even out over five years.”

These four pillars reinforce each other in Sifter’s view, and are therefore always assessed together.

“Growth without high ROIC destroys value,” Korpinen says. “ROIC without growth limits compounding.

“Strong financials without a competitive advantage are temporary. And high quality at any price can lead to poor returns.”

The firm is also deliberate about staying within it’s “circle of competence” in terms of the opportunities it identifies.

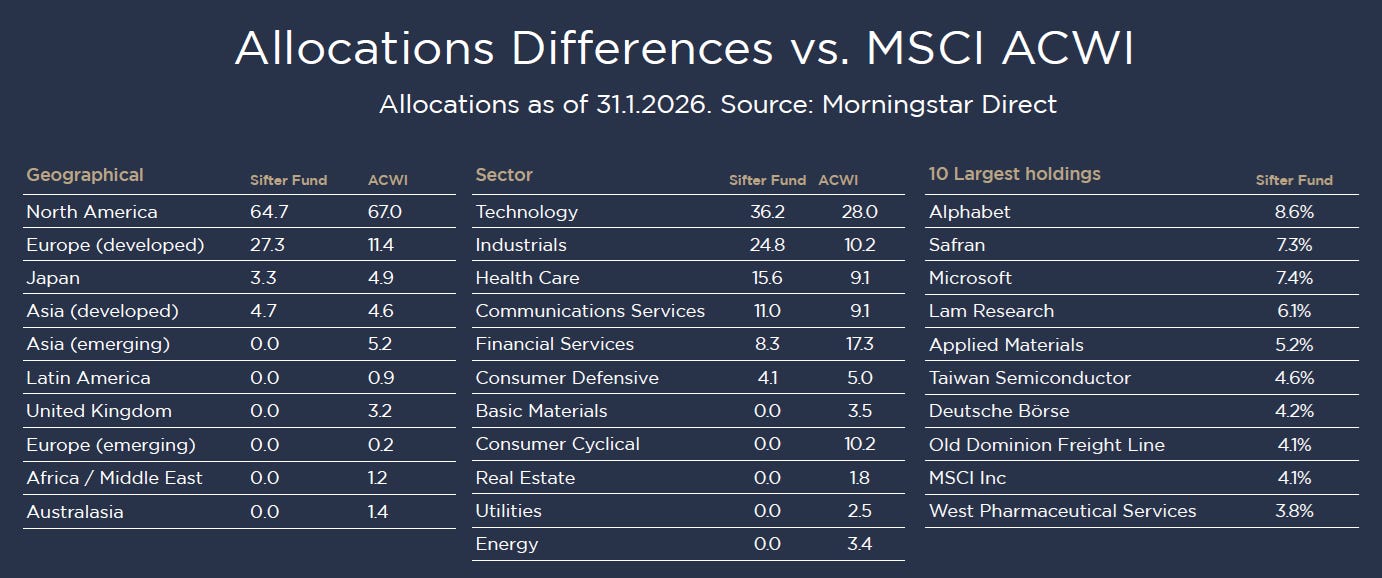

“We don’t invest in areas we are not comfortable or familiar with like banks, raw materials and energy,” Korpinen says. “We emphasise technology, industrials and healthcare where we tend to find quality more often than in other sectors.”

Notably, just under 25% of the fund is held in industrials stocks, which is more than twice the weighting of this sector in the MSCI ACWI. Korpinen notes that this also sets them apart from most other quality managers.

“We do have a bit of a different view on quality,” he points out. “The best evidence of that is that if we compare our portfolio to the global quality index or other quality funds, the common holdings are less than 20%.

“We have engineering backgrounds, so it may be our bias as well, but at least we have been consistent in that bias. Roughly 80% of the portfolio companies are predominantly B2B businesses. Those are the kinds of businesses we find in technology and industrials.”

An example is French aircraft engine manufacturer Safran. It has a 70% market share in the narrowbody engine market.

“It has a great moat because you don’t really make money when you develop these engines,” Pöyhönen says. “It can take a decade from development to use.

“You don’t even make that money selling the engines. You only really make money by maintaining them, and that’s where Safran has a dominant position.”