“The opportunity cost of low volatility can be quite high”

Marriott’s Lourens Coetzee talked me through the way the firm approaches managing its multi-asset income fund that has one of the longest and most impressive track records in the industry.

The Marriott Core Income Fund launched more than two decades ago. This was before the multi-asset income category was even created, and before this type of strategy was anywhere near as popular as it is now.

Marriot has always managed the strategy as an asset allocation portfolio, looking to deliver high levels of income at low levels of risk. Since inception it has returned just shy of 10% per annum, and over the past 10 years it has consistently been one of the top-performing multi-asset income unit trusts in South Africa.

Marriott’s Lourens Coetzee (pictured below) believes that one of the reasons behind this track record is that they do not consider volatility to be the fundamental measure of risk.

“We prefer to think about risk for an income fund as outcome risk and liquidity risk”

“We look at risk slightly differently to the market,” Coetzee says. “We don’t consider volatility as the primary risk in the income fund sector. The main reason is because if fixed interest investment are held to maturity and the issuer meets its obligations, short-term price movements don’t affect the outcome. Secondly a big part of the investible universe – corporate credit – isn’t trading efficiently.

“We prefer to think about risk for an income fund as outcome risk and liquidity risk,” he adds. “The big questions we ask ourselves are, first of all, you going to get your money back? And, secondly, can you get liquidity when you need it? Those are the risks you really face.”

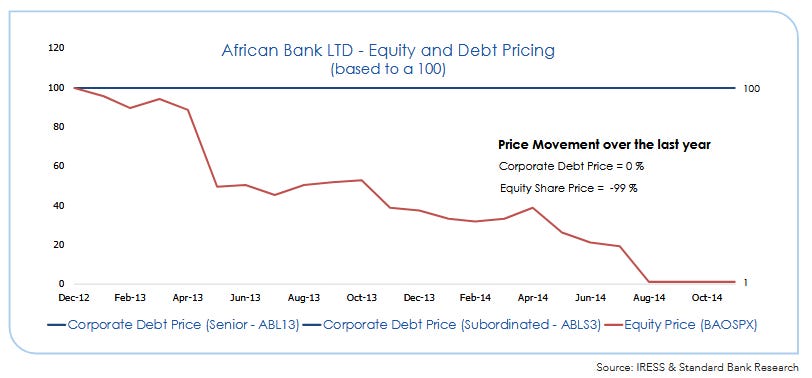

He believes that credit risk in particular is easily underestimated in an environment where assets are not pricing effectively. This was most obviously illustrated in 2014 when shares in African bank had fallen 99% before the business was placed under curatorship, but the price of its bonds didn’t move.

If anything, Coetzee adds that credit risk has become even more imperative to consider in the current environment.

“Slow economic growth combined with high borrowing costs are not great because companies generally struggle. This makes it harder to pay back their loans. So, as a manager, understanding the risk that a company might not pay back its loans is especially critical now.

“More recently, we have seen some corporate failures, with a notable one being in the taxi industry, and this has negatively impacted a number of income funds. Unfortunately, investors did not understand the risk they were exposed to as disclosures were poor and the pricing inefficiency of the corporate credit market certainly didn’t help.”

“What happened with African Bank and Bridge Taxi Finance bonds shouldn’t happen”

Coetzee notes that the Association for Savings and Investment South Africa (ASISA) has picked up on this, which led to it issuing recommendations last year that managers should disclose all the risks in their portfolios.

“What happened with African Bank and Bridge Taxi Finance bonds shouldn’t happen,” Coetzee says. “Even if the market price of the bonds didn’t move, as the asset manager you should look to ensure all investments are fairly priced.”

This doesn’t mean that Marriott avoids corporate paper. A decade ago, the fund had a high exposure to credit and held no government bonds. Coetzee (pictured below) explains that during that period, investors were rewarded for taking on additional credit risk. Additionally five-year bank deposits were offering yields comparable to those of 10-year government bonds. As a result, there was little incentive to take on the extra risk associated with more duration.

But he adds that they have always placed a high hurdle on what they will buy.

“We restrict ourselves to only lending to corporates that form part of our investible universe,” Coetzee says. “Those are companies that have the ability to pay reliable dividends. With these corporates, we have no real concern over whether we will get our interest payments because you get paid interest before dividends, and we’re very confident that these companies will be paying dividends.”

The fund currently has approximately 40% exposure to quality corporate debt with no exposure to borrowers with a credit rating below A+. Coetzee adds that this isn’t just limited to financial services firms, but also includes the bonds of some property companies, and the likes of Bidvest, Pepkor and Netcare.

Source: Marriott (as at 31 May 2025)

“We’re happy to have exposure to good quality corporate debt where we get a bit of pickup over cash,” Coetzee says. “We pride ourselves on the fact that we have not had a default event in the history of managing our income funds.”

With yields from South African bonds being so attractive, Coetzee also believes there is no need to take excessive credit risk at the moment.

“The Core Income Fund’s ideal investment term is two years, and this gives us the ability to accept slightly higher levels of duration,” he says. “Our neutral position is to have duration of between one and two, but we have a self-imposed limit to not go above four.

“In extreme moments we can move above our neutral position, like we did in Covid when we could buy six-year government bonds at yields as high as 12%. We moved approximately 40% of the fund into those. We think you have to take advantage of those kinds of massive opportunities.

“The opportunity cost of low volatility can be high,” Coetzee adds. “This fund can be a bit more volatile than other funds from time to time. What is important though is to deliver good outcomes for investors over a two-year period and we know by restricting our exposures to investments that are able to pay both their interest and principle back, we are not taking undue risk.”